Bonds – Risk analysis and simulation

Actions – Risk analysis and simulation

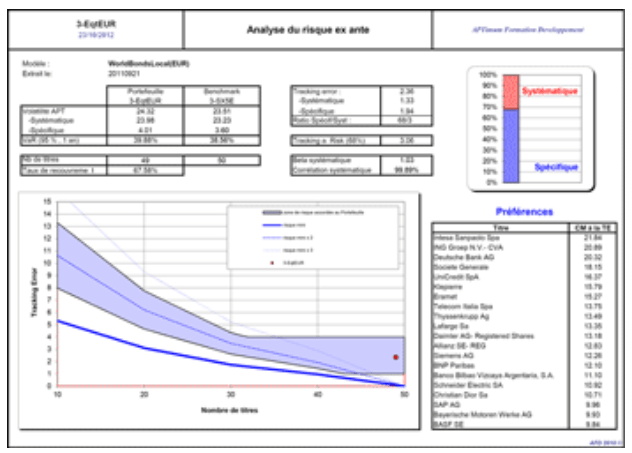

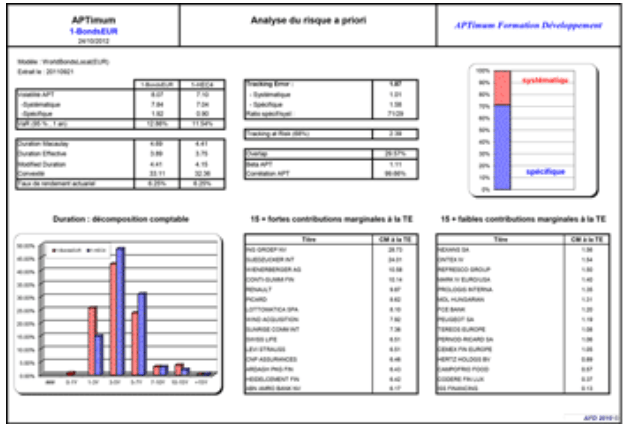

Bonds – Risk analysis and simulation

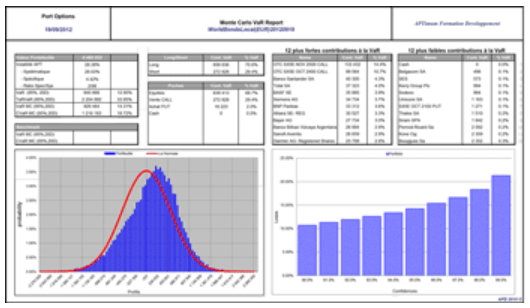

APT Monte Carlo: Simulation

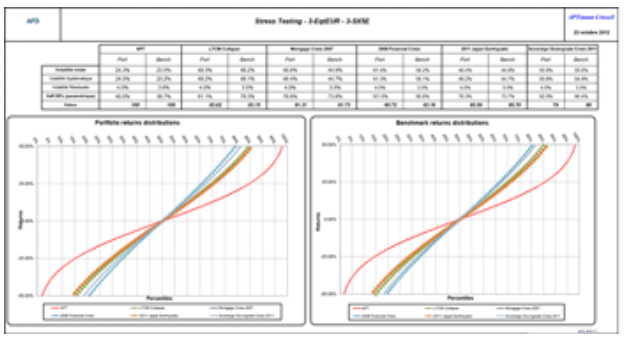

Stress Testing and Scenario Analysis – Analysis

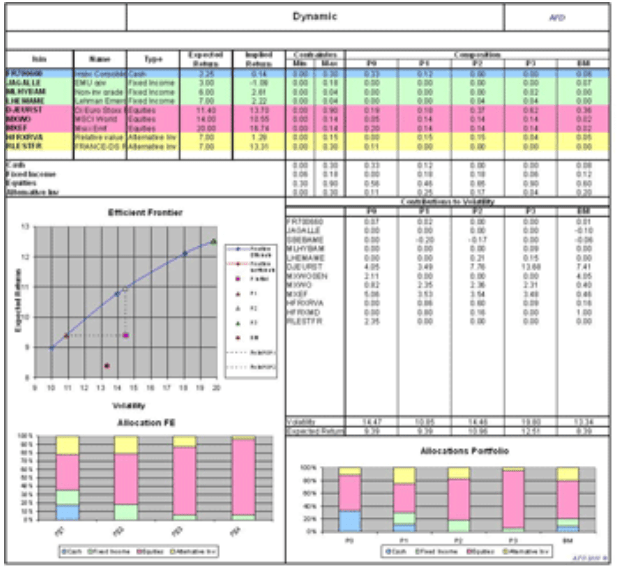

Efficient Frontier – Analysis

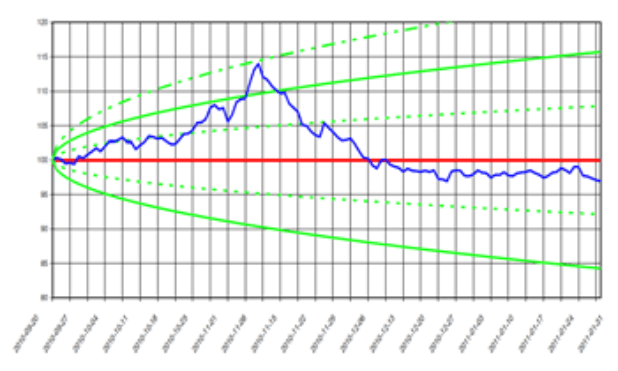

Performance vs. Risk – Analysis

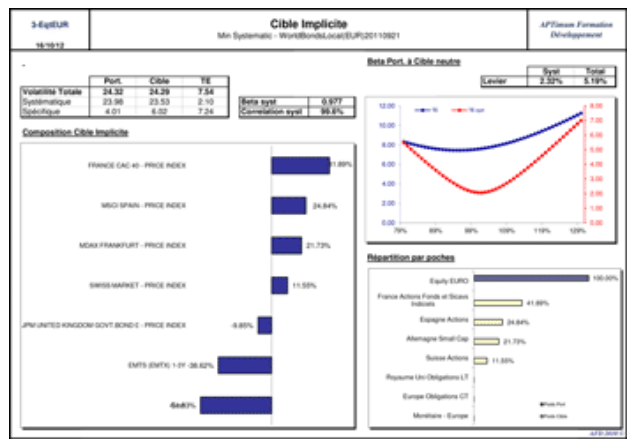

Implicit target – Identification

Proxy Hedge Fund – Construction

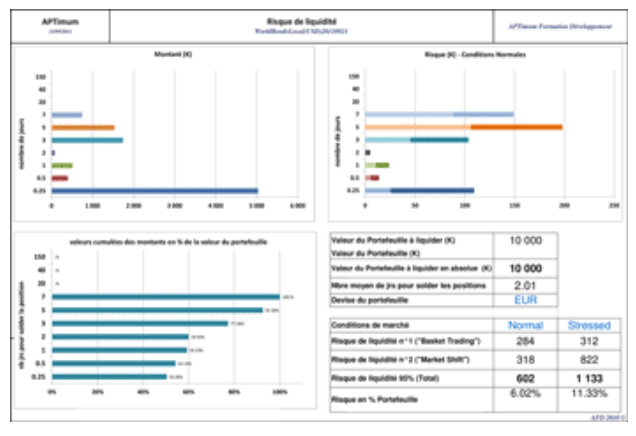

Liquidity – Risk analysis

Promoters: Risk analysis and performance

of external funds

Historical Fund Analysis: Risk Analysis

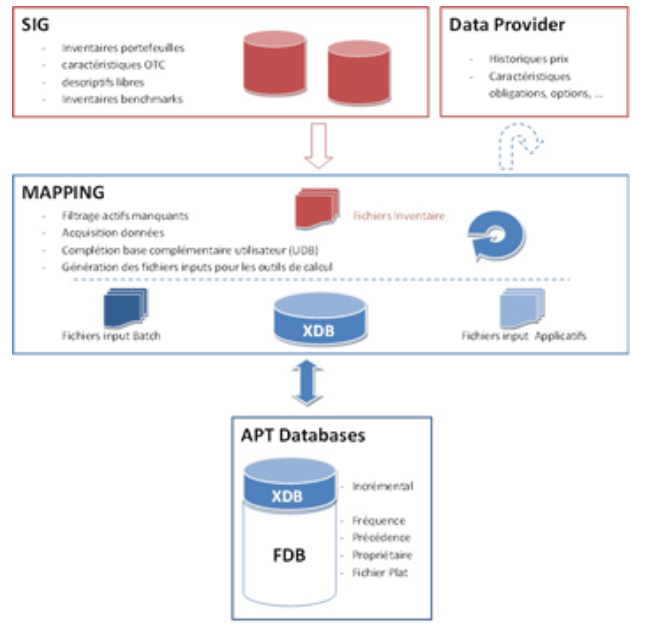

- Verification of asset recognition

- Modeling of missing instruments

- Integration into user architecture (GIS, Data Provider and other databases)

- Analysis of absolute and relative equity portfolio risk with all relevant indicators;

- Accounting decomposition;

- Accounting risk attribution;

- Behavioral attribution;

- Analysis of marginal and total risk contributions per position.

- Absolute and relative risk analysis of the bond portfolio with all relevant indicators including actuarial calculations;

- Accounting decomposition;

- Accounting attribution of risk;

- Behavioral attribution;

- Analysis of marginal and total contributions to risk by position.

- Complete analysis of portfolio behavior after impact of selected volatility and level shocks;

- Selection of historical or customized scenarios;

- Effect splitting by explanatory variables.

- Presentation of the efficient frontier and the initial portfolio and benchmark for a given profile;

- Presentation of portfolio compositions within the efficient frontier;

- Risk breakdown of each efficient portfolio.

- Monitoring relative performance within risk envelopes;

- Decision-making tool for arbitrages;

- Quantifies the manager’s contribution to portfolio performance.

- Construction of a combination of indices (or securities) with the risk profile closest to that of the initial portfolio;

- Optimization with or without constraints (Min/Max weight, number of securities, Tracking Error optimization, Tracking-At-Risk®, etc.).

- Reproduction of the risk profile of an alternative fund (or fund of funds), based on a composition of alternative indices quoted on a daily basis;

- Composition of the implicit target and the APT correlation achieved;

- Effect splitting by explanatory variables.

- Evaluation of the possible loss in the event of liquidation of all or part of the portfolio;

- Calculation complies with UCITS IV regulations on liquidity risk.

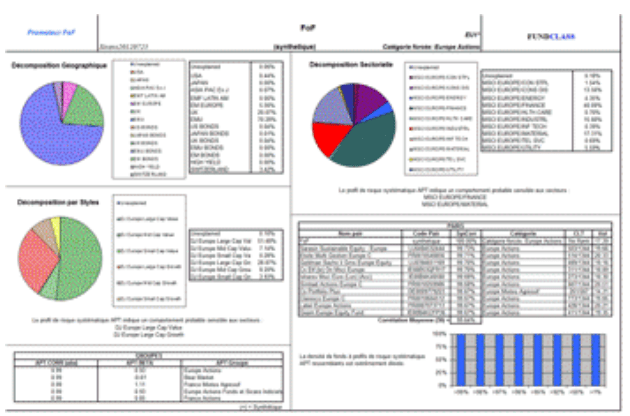

- Reconstitution of the sensitivities of funds or funds of funds to geographic, sector and style variables;

- Calculations based on fund net asset values;

- Possibility of presenting the fund’s systematic Beta/correlation pairs with peer groups established by our partner FUNDCLASS.

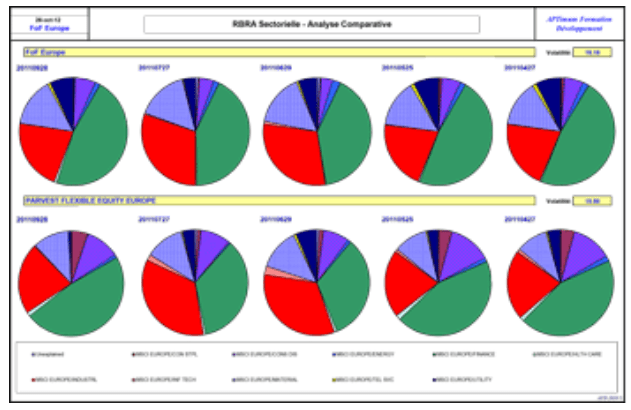

- Complementing the Promoters analysis – similar analysis on a historical basis;

- Historical analysis of sensitivities and selected strategies;

- Independent risk allocations showing correlations and Betas of funds against a set of indices/strategies.

Complementing the Promoters analysis – similar analysis on a historical basis;

Historical analysis of sensitivities and selected strategies;

Independent risk allocations showing correlations and Betas of funds against a set of indices/strategies.